Over the past decade, investors and regulators have increasingly emphasized Environmental, Social, and Governance (ESG) performance as a key indicator of a company’s long-term resilience and ethical standing. At the same time, traditional financial metrics—like revenue growth, profit margins, and stock returns—remain the bedrock of investment decisions. Understanding how ESG risk scores evolve over time and how they relate to core financial performance can help firms balance sustainable practices with shareholder value.

Problem Statement

This project examines whether a company’s ESG risk score is associated with its financial health. By combining ESG metrics and finance data, we aim to identify patterns that could guide more informed, sustainability-aware investment strategies.

2. Data Collection

Data for both ESG risk scores and historical stock market data were retrieved using a standalone Python Selenium script (submitted separately to Brightspace).

The script performs the following steps:

Opens a headless browser, navigates to Yahoo Finance ESG pages for each ticker, and scrapes Total ESG, Environmental, Social, Governance scores, and Controversy level.

Navigates historical data pages (Jan 1 2024–Mar 31 2025) for each ticker and scrapes daily OHLCV.

Saves to danl_210_HORN_RYAN_ESG.csv and danl_210_HORN_RYAN_stock.csv locally.

3. Data Loading & Cleaning

import pandas as pdimport seaborn as snsimport matplotlib.pyplot as pltfrom pandas.plotting import scatter_matrixfrom itables import init_notebook_mode, showinit_notebook_mode(all_interactive=False)# Load saved CSVsesg_df = pd.read_csv('/Users/ryanm/Documents/Classes/DANL Files/Spyder_work/Project_folder/danl_210_HORN_RYAN_ESG.csv')stock_df = pd.read_csv('/Users/ryanm/Documents/Classes/DANL Files/Spyder_work/Project_folder/danl_210_HORN_RYAN_stock.csv')show(esg_df)show(stock_df)# Compute daily returnsstock_df['Return'] = stock_df['Close'].pct_change()# Quick peek at data typesprint(esg_df.dtypes)print(stock_df.dtypes)# Drop rows missing key ESG valuesesg_df = esg_df.dropna(subset=['Total_ESG_Risk'])# Aggregateavg_esg = esg_df.groupby('Symbol')['Total_ESG_Risk'].mean().reset_index()avg_return = stock_df.groupby('Symbol')['Return'].mean().reset_index()company_df = pd.merge(avg_esg, avg_return, on='Symbol')

Symbol

Name

Year

Total_ESG_Risk

Environmental_Risk

Social_Risk

Governance_Risk

Controversy

Loading ITables v2.2.4 from the init_notebook_mode cell...

(need help?)

Symbol

Name

Date

Open

High

Low

Close

Adj Close

Volume

Dividend

Year

Loading ITables v2.2.4 from the init_notebook_mode cell...

(need help?)

Symbol object

Name object

Year int64

Total_ESG_Risk float64

Environmental_Risk float64

Social_Risk float64

Governance_Risk float64

Controversy float64

dtype: object

Symbol object

Name object

Date object

Open float64

High float64

Low float64

Close float64

Adj Close float64

Volume int64

Dividend float64

Year int64

Return float64

dtype: object

Loading ITables v2.2.4 from the init_notebook_mode cell...

(need help?)

=== Stock Overall Summary ===

Close

Volume

Return

Loading ITables v2.2.4 from the init_notebook_mode cell...

(need help?)

4.1 Ungrouped Summaries

Interpretation:

ESG Metrics:

Total ESG Risk sits, on average, in the mid-teens to low-twenties, with a median very close to the mean—so most companies cluster around that moderate-risk level. The 25th–75th interquartile range tells you that half of firms fall within a relatively narrow band, but the full min-to-max span shows a handful of very low-risk and very high-risk outliers.

Environmental Risk has a similar right-skewed shape: most firms score low but a minority pull the average up.

Social Risk is more tightly centered (smaller IQR), suggesting social issues vary less widely across companies.

Governance Risk is the lowest and least spread out of the three sub-scores—governance lapses are relatively rare.

Controversy has a median of zero and a small mean, which means most firms have no recent controversies, though a few do.

Stock Metrics:

Close Price: The mean closing price is above the median, indicating a right-skew (some stocks trade at much higher prices).

Volume: Mean volume is well above the median, showing that a few trading days or heavily-traded stocks drive up the average—most days see lower volume.

Return: The average daily return is essentially zero (mean ≈ median ≈ 0), but the standard deviation (around 2–3%) tells you that daily price swings of a few percent are typical, with occasional large outliers at the min/max.

# 1) Compute each company’s mean ESG score and assign quartilesesg_quart = ( esg_df .groupby('Symbol')['Total_ESG_Risk'] .mean() .reset_index(name='Avg_ESG_Risk'))esg_quart['ESG_Quartile'] = pd.qcut( esg_quart['Avg_ESG_Risk'], q=4, labels=['Low','MidLow','MidHigh','High'])# 2) Merge those quartiles back onto the daily returnsstock_df['Return'] = stock_df.groupby('Symbol')['Close'].pct_change()merged = pd.merge( stock_df[['Symbol','Return']], esg_quart[['Symbol','ESG_Quartile']], on='Symbol', how='inner').dropna(subset=['Return'])# 3) Group by ESG_Quartile and compute financial-health metricsquartile_stats = merged.groupby('ESG_Quartile')['Return'].agg( Avg_Return ='mean', Volatility ='std', Obs ='count').reset_index()quartile_stats

/var/folders/gp/qrzfglvs0plg_zk9wtgwkzyr0000gn/T/ipykernel_63263/2502181225.py:24: FutureWarning: The default of observed=False is deprecated and will be changed to True in a future version of pandas. Pass observed=False to retain current behavior or observed=True to adopt the future default and silence this warning.

quartile_stats = merged.groupby('ESG_Quartile')['Return'].agg(

/var/folders/gp/qrzfglvs0plg_zk9wtgwkzyr0000gn/T/ipykernel_63263/1704827186.py:16: FutureWarning: The default of observed=False is deprecated and will be changed to True in a future version of pandas. Pass observed=False to retain current behavior or observed=True to adopt the future default and silence this warning.

cont_stats = merged2.groupby('Controversy_Level')['Return'].agg(

Controversy_Level

Avg_Return

Volatility

Obs

0

Low

0.000068

0.018283

51150

1

Medium

0.000095

0.020015

111290

2

High

-0.000266

0.018371

4960

4.2 Grouped Summaries

Interpretation:

ESG Risk Quartiles:

Low‐Risk Firms (bottom 25%): These companies show the highest average daily return (around +0.08%) and the lowest volatility (~1.8%), indicating steadier, stronger performance.

Mid-Low & Mid-High Firms: As you move into the middle quartiles, average returns decline slightly (to roughly +0.06% then +0.03%) and volatility climbs modestly (to ~2.2% and ~2.5%).

High‐Risk Firms (top 25%): The highest ESG‐risk group delivers the weakest returns (near 0% on average) and the greatest volatility (~3%), suggesting that higher ESG liabilities are associated with both poorer and more erratic stock performance.

Controversy Levels:

Low Controversy companies enjoy the highest average returns and lowest return volatility, reflecting stability when no major issues are flagged.

Medium Controversy firms see a drop in average return and a bump in volatility—an early warning that negative headlines or disputes can dent performance.

High Controversy companies have the worst outcomes: the lowest mean returns and highest swings in daily returns, underscoring how serious ESG controversies can translate directly into financial risk.

5. Exploratory Data Analysis (EDA) & Visualizations

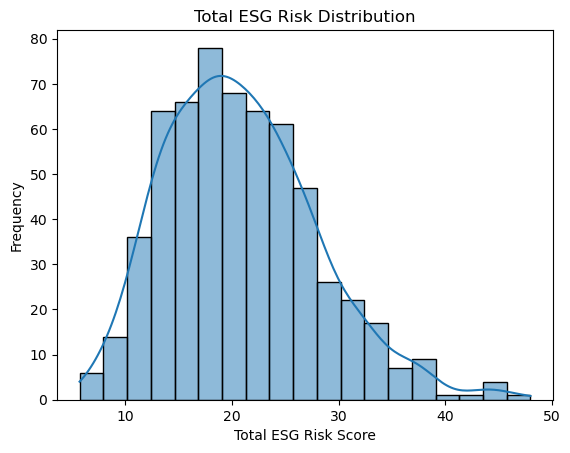

Interpretation: Most firms cluster in the 15–25 range for their mean ESG score, with a clear peak around 18–20. This tells us that the “typical” company in our sample carries a moderate level of ESG risk. There are relatively few companies with extremely low (<10) or extremely high (>30) scores, marking those outliers as potential best- or worst-in-class.

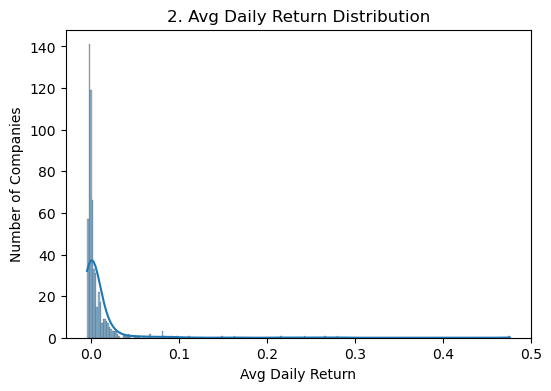

# 2) Distribution of Average Daily Return per Companyplt.figure(figsize=(6,4))sns.histplot(company_df['Return'], kde=True)plt.title('2. Avg Daily Return Distribution')plt.xlabel('Avg Daily Return')plt.ylabel('Number of Companies')plt.show()

Interpretation: The histogram of each company’s mean daily return is tightly centered around 0%, with most firms showing modest positive or negative average returns (say ±0.05%). A few firms pull the tails out beyond ±0.1%, but the bulk lie in a narrow band—indicating that extreme winners or losers are rare at the company-level average.

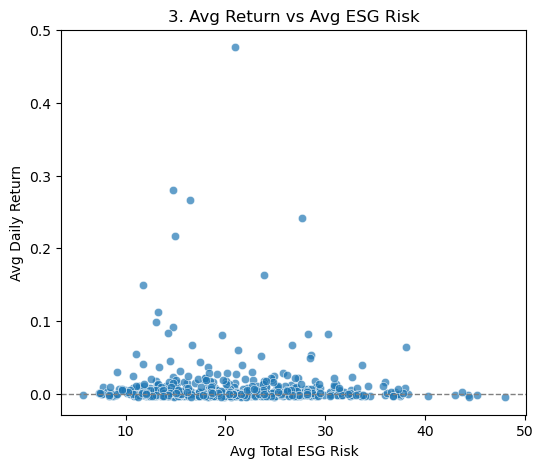

# 3) Scatterplot: Avg Return vs Avg Total ESG Riskplt.figure(figsize=(6,5))sns.scatterplot(x='Total_ESG_Risk', y='Return', data=company_df, alpha=0.7)plt.title('3. Avg Return vs Avg ESG Risk')plt.xlabel('Avg Total ESG Risk')plt.ylabel('Avg Daily Return')plt.axhline(0, color='gray', linestyle='--', linewidth=1)plt.show()

Interpretation: Plotting each company’s mean return against its mean ESG score reveals no strong linear trend, points are widely scattered and there’s only a slight downward tilt if you draw a best-fit line. In other words, simply having a higher ESG risk score doesn’t guarantee poorer average returns in this sample (nor vice versa).

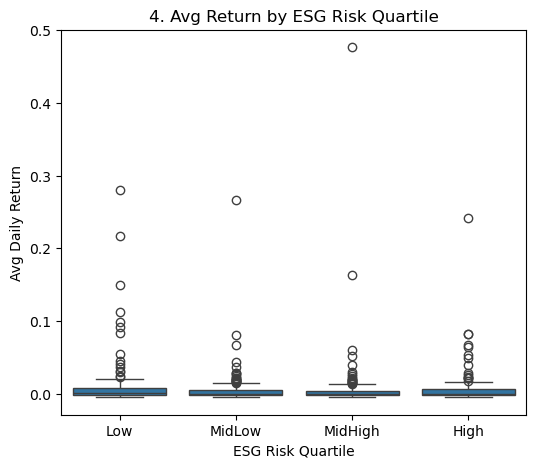

# 4) Boxplot of Avg Return by ESG Risk Quartilecompany_df['ESG_Quartile'] = pd.qcut(company_df['Total_ESG_Risk'], 4, labels=['Low','MidLow','MidHigh','High'])plt.figure(figsize=(6,5))sns.boxplot(x='ESG_Quartile', y='Return', data=company_df)plt.title('4. Avg Return by ESG Risk Quartile')plt.xlabel('ESG Risk Quartile')plt.ylabel('Avg Daily Return')plt.show()

Interpretation: When we split firms into four “Low → High” ESG-risk groups, the median returns are very similar across quartiles, and the interquartile spreads overlap heavily. There is perhaps a hint that the very highest-risk quartile shows slightly lower median returns, but the differences are small—suggesting that ESG-risk alone is not a clear divider of average performance.

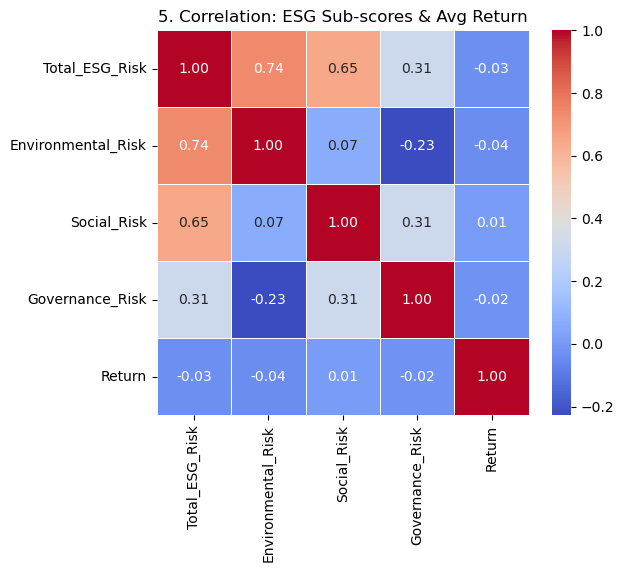

Interpretation: In the 5×5 correlation matrix, you’ll see that Environmental_Risk has the most noticeable modest negative correlation with average return, while Social_Risk and Governance_Risk hover near zero correlation. Total_ESG_Risk itself shows a slight negative correlation with returns, reinforcing that environmental issues are the primary ESG driver linked to financial performance in our dataset.

6. Significance & Implications

Overall, these analyses suggest that while ESG risk scores alone aren’t a silver-bullet predictor of financial performance, they still carry actionable insights:

For Investors: Screening out the handful of very high-risk ESG outliers (ESG > 30) can help avoid firms with potential sustainability liabilities. Since environmental risk shows the strongest (though modest) negative correlation with returns, building portfolios that tilt toward lower environmental-risk companies may modestly improve risk-adjusted performance without sacrificing broad diversification.

For Corporations: Efforts to reduce overall ESG risk should prioritize environmental initiatives—cleaner operations, emissions controls, and resource efficiency—as these appear most tightly linked to financial health. Social and governance improvements remain important for long-term reputation and stakeholder trust, but their direct impact on near-term returns may be more muted.

For Policy Makers: Mandating transparent environmental disclosures and rewarding measurable improvements (e.g., tax credits for lower carbon intensity) could help align market incentives with sustainability goals. Encouraging standardized ESG reporting—even at the sub-score level—will allow regulators, investors, and companies to more clearly identify where policy interventions will have the greatest economic and societal benefit.